You Need an Estate Plan

If you are reading this, you probably need an estate plan.

If you have children, live in states like California, you owe it to your family to have an estate plan that includes a revocable trust.

This is a great time to also remind you that in addition to not being a financial advisor, I am also not a lawyer. This post isn’t legal advice or financial advice...

What’s In An Estate Plan?

One of the first things I did after my daughter was born 6 years ago was set up an estate plan. While the specifics of what is included in an estate plan will be different for everyone, mine involved the following legal documents (with my layman explanation):

Revocable Trust: A legal arrangement that lets me and my partner manage our assets while we are alive. It establishes the rules and powers the trust has, while also allowing assets controlled by the trust to bypass probate if both my wife and I pass.

Certification of Trust: A summary of the trust that I have needed to use anytime I set up a new account in the trust’s name.

Last Will and Testament: A legal document that provides more specific instructions on what happens after I pass and importantly allows me to specify the specific guardianship plan for my daughter.

Advance Healthcare Directive: Specifies who can make healthcare decisions for me if I am incapacitated as well as my specific wishes around my preferences to be unplugged and cremated.

Durable Power of Attorney: grants a trusted person the authority to manage my financial and legal matters if I become incapacitated.

HIPAA Release: Authorizes healthcare providers to share my medical information with designated individuals, ensuring they have access to necessary health records.

Spousal Property Agreement: Document that specifies that our household assets are community property, however California defines it.

This stuff is complicated. What makes it so important?

Each of these documents is important. Since this is FAANG FIRE, I am going to focus on the financial pieces. One major one for me is a revocable trust’s ability to bypass California probate court.

Probate: A legal process that determines what should be done to with your assets, guardianship of minors, and more after you die. The specifics and rules governing the process are different in each state.

Two Big Reasons to Avoid Assets Going to Probate in California

On average it takes a year and a half! This means that your family may not have access to your assets for 1.5 years!

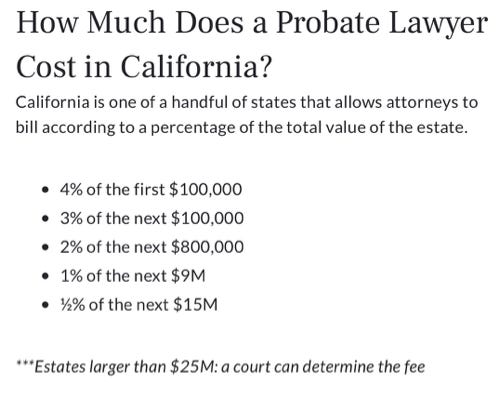

There are significant fees which are mandated by California

So if your estate has assets totaling $5,000,000 the impact of probate could be:

4% of the first $100,000: (.04 x 100,000) = $4,000

3% of the next $100,000: (.03 x 100,000) = $3,000

2% of the next $800,000 (.02 x 800,000) : = $16,000

1% of the remaining $4M: (.01 x 4,000,000) = $40,000

Bringing your total probate lawyer costs to $63,000. Also important to note that this is on the value of your assets. Which means even if your $3,000,000 home has a $2,000,000 mortgage on it when you pass, the state will calculate the fees based on the $3,000,000!

This isn’t unique to California either, be sure to understand how your state’s probate process works.

Rules of Guardianship

The stakes are even higher when children are added. This is a major reason why I wanted to set up my estate plan to begin with so soon after my daughter was born. Part of the estate planning process involved clearly spelling out who will take over guardianship of my daughter. Who will be the executor of the estate that I trust to make decisions. What rules I have to distribute my assets.

Three Tiers of Estate Plan Services

Now that we understand why we might want an estate plan, how do you actually go about getting one?

Like many things, there are multiple tiers of services out there ready to help you establish your estate plan. They range from self-serve through to having specialized teams of lawyers. I’ll talk through how I went about creating mine as well as other options that are out there.

Estate Plans Tier 1: Employer Legal Benefit

Many tech companies offer estate planning as part of a legal benefit, either as a free perk or an optional cost during open enrollment. This is the route I took when I first set up my own estate plan.

The process started with needing to call several lawyers from a provided list just to see if they could create an estate plan under my company’s legal benefit. Each law firm seemed to include very different offerings, fees, and unclear up-charges. Navigating this felt like dealing with a black box. I was concerned about randomly being upsold something I didn’t need.

After multiple calls I found a firm that didn’t charge for notary, didn’t charge for adding specific clauses, didn’t charge me for follow up emails. As part of the legal benefit you get a fairly cookie cutter estate plan. That was fine for me. I didn’t own any property. I only have one kid. I didn’t have any complicated needs.

The process involved filling out a series of forms and attending an in-person office visit for preliminary information gathering. A month later, I received a draft of the documents, which included typos in names, incorrect addresses, and listing the city as Alameda instead of San Francisco—small errors that were not very confidence-inspiring. Nonetheless, I pressed on, and they were quick to make edits and corrections.

Another month later, everything was approved, and my wife and I (with our six-month-old in tow) visited the office to sign all the documents in the presence of a notary. After that, I was set—kind of. I now physically had an estate plan. However, having an estate plan alone doesn't help me avoid the probate costs that were my primary motivation for setting up a trust in the first place.

I still needed to go through the process of re-titling every bank account and brokerage account to be owned by my trust and not owned by me, as well as changing beneficiaries on different retirement plans to ensure the secondary beneficiary was the trust (the first being my wife). If I owned any property I would also need to go through the trouble of retitling the property into the name of the trust vs my own name. Fortunately, we didn’t need to do that.

In the end, I did have an estate plan and trust. Most of my taxable accounts were titled in the name of the new living trust! It was a process, but I was happy to have finished it.

That's the Tier 1 experience—something to consider if your employer plan includes it, especially if you have a simple situation like mine. I would also categorize all the up-and-coming startups entering this space within this first tier.

If your situation is more complex, if the Tier 1 process sounds too arduous, or if you are on a time crunch that is causing you to delay creating an estate plan, I encourage you to explore the next tiers of options that can make the process easier and more personalized.

Estate Plans Tier 2: Guided Estate Planning Services

The second tier of estate planning bridges the gap between the cookie-cutter solutions of Tier One and specialized legal expertise of Tier Three. This level provides additional expertise and guidance throughout the entire process, including help with all the follow-up tasks that are critical to actually getting the benefits from setting up an estate plan!

Now is also the perfect time to introduce today’s sponsor Twin Peaks Estate Services who falls within this second tier.

This post is sponsored by Twin Peaks Estate Services

At Twin Peaks Estate Services, we provide a white-glove, done-with-you solution for your basic estate planning needs. Our team guides you through every step, helping you define your wishes with care. In 21 days or less, we can have your documents prepared, notarized, and trust funded*. Click below to schedule a complimentary Estate Planning consultation and be one step closer to peace of mind.

*Timeline varies on complexity

Check them out at www.twinpeaksestateservices.com

I asked brothers Vishal and Tushar Kumar of Twin Peaks Wealth Advisors a few questions about when a FAANG employee might want to explore estate planning options beyond those offered as an employee perk.

In your experience who benefits the most from that second tier of estate planning?

People who benefit the most value time (speed of execution) and accountability (someone to ensure they see this to the finish line). If you want to delegate the ownership/burden of getting your estate planning to someone, this service could make sense.

What are the most common shortcomings of the estate plans that often come from employee benefit legal plans?

The main one is that these plans may not help with proper funding of the trust once it is established. Some will help with moving your home to the trust, but almost none of them will help you with other assets (stock plans, brokerage accounts, bank accounts, college funds, etc). Our service will help with the funding of the trust as well. We will sit with our clients on Zoom to retitle accounts, add beneficiaries, and put together a list of any follow-up items that they're responsible for (example: go to your local bank with a copy of your trust certification and ask them to retitle your account).

That second point so critical. I have talked with a number of peers who went through the trouble of getting a revocable trust created as part of the estate planning benefit without doing the most important step of funding the trust! I am guilty of this too! As part of writing this article I realized that despite setting up my trust 6 years ago I was still missing beneficiaries on some of my accounts (and including the trust as a contingent on others)!

Other Shortcomings of Tier 1

Limited Customization: These plans typically offer basic templates or one-size-fits-all solutions, which may not account for unique family dynamics, blended families, or complex asset structures.

Lack of Continuity: Employer-sponsored plans may not support updates over time. Estate plans require periodic reviews to stay relevant, but ongoing support might be limited or not included, which can be problematic when life events occur, such as marriage, the birth of children, or changes in wealth.

Limited Beneficiary Designations: For individuals with complex needs, such as charitable giving, multi-generational planning, or business succession, employer-sponsored plans rarely offer the detailed customization required.

Inadequate Integration with Overall Financial Plan: Estate plans should work in harmony with broader financial goals, like retirement planning, tax strategies, and wealth transfer goals. Employer-sponsored plans often operate independently, missing this critical holistic approach.

Limited Geographic Relevance: Laws governing estate planning vary widely by state, and employer-sponsored solutions may not address state-specific laws, which could lead to outdated or unenforceable documents if they don’t comply with local legal standards.

Privacy Concerns: Employees may feel uneasy about sharing personal information through employer-sponsored programs, especially if there are any conflicts with company interests or privacy policies.

Tier Two acts as a bridge between basic cookie-cutter solutions and the expertise of specialized lawyers. It combines speed, education, guidance, and assistance to create a more tailored and comprehensive estate plan.

Tier 3 and Beyond

There is an entire world beyond these initial two tiers.

Much of the content thus far was focused around foundational estate planning documents with straightforward outcomes. With “living” revocable trusts that you can easily modify. The realm of estate planning gets infinitely more complex as the complexity of needs grows, or if your assets have grown well beyond estate tax limits.

Particularly as you begin utilizing estate planning for asset protection and complex tax planning above the estate tax limits.

Here are examples of some more complex trust needs that would likely be best managed by an estate attorney who specializes in these types of trusts.

Special Needs Trusts: I have friends who have utilized SNTs to ensure their dependents maintain eligibility for various government benefits and protect their financial needs long term.

Irrevocable Trusts: Unlike revocable trusts, these can not be altered once set up, but can often come with estate tax planning benefits.

Generation Skipping Trusts: A flavor of irrevocable trust designed to transfer assets to grandchildren (skipping a generation), minimizing potential long term estate taxes (the alternative would be the parents paying the estate tax at the death of their parents, with the grandchildren paying estate taxes again once their parents pass).

If you are interested in this path, I really appreciated this article on Family Health Report which broke down how to even begin approaching the interview process for finding an estate planning lawyer who is the best fit for your specific situation.

Questions the authors recommend asking:

How much of the practice of the lawyer you’re interviewing is dedicated to trust and estate work?

In which jurisdictions, in addition to the one where the lawyer is resident, do they work most extensively?

What differentiates this firm from its competitors in the trust and estates practice?

What is the median and average range of wealth, and typical number and generations of family members of your estate planning clientele?

Are the lawyer’s clientele characterized by a specific attribute: concentrated positions, active business ownership, financial assets, cryptocurrency, or other narrow profile?

What are the essential near-term and longer-term priorities in an engagement of our size?

How does this lawyer discern/distill/define the client’s priorities?

How do they incorporate the client’s priorities into their process, matching technical solutions with family values and dynamics?

Do they have an overarching philosophy regarding dynasty and other generation-skipping trusts’ design, and jurisdiction selection for these entities?

Stop Procrastinating!

If you are a FAANG FIRE subscriber there is a high probability that you have a high income, have a high net worth, are married, live in California/New York, and have kids. You are the type of person who would most benefit by having an estate plan set up.

This is also not something to set and forget. You should be revisiting your documents anytime your situation changes. Did you move to a different state? Purchase more property? Have a child? Have a change in your guardianship plans? No longer on speaking terms with your executor? Like perhaps you realized you don’t want your anti-vax sibling in charge of your health care directive?

Make your heirs’ lives easier and spend the time now to protect them. I know it can feel morbid to think about what happens after you pass away, but it is an important piece of any good plan. You can potentially save your loved ones a significant headache during a time when they are already mourning!

How did you know I was just researching about an estate plan!? :) I have a first appointment with an estate planning attorney later today. Your post was very timely and informative. Thanks for everything you do!

Should/Can you put yourself as the trustee of the trust? For the revocable living trust?

Can you share more of the people involved in the trust as an example? (trustee/beneficiary/etc...?)

When you go to the notary with the beneficiary (e.g. wife)

> "Another month later, everything was approved, and my wife and I (with our six-month-old in tow) visited the office to sign all the documents in the presence of a notary."

Does that imply your beneficiary/wife/(trustee?) have visibility of all your assets?

Or is the signed document doesn't mention any specific amounts? bank accounts?

Or visibility is only available after death?